War and logistics disruptions in the Strait of Hormuz send fertilizer prices soaring, raising the risk of another food-price rebound in Mexico

Higher prices for urea and other imported inputs threaten to push up farm costs and gradually feed into food inflation.

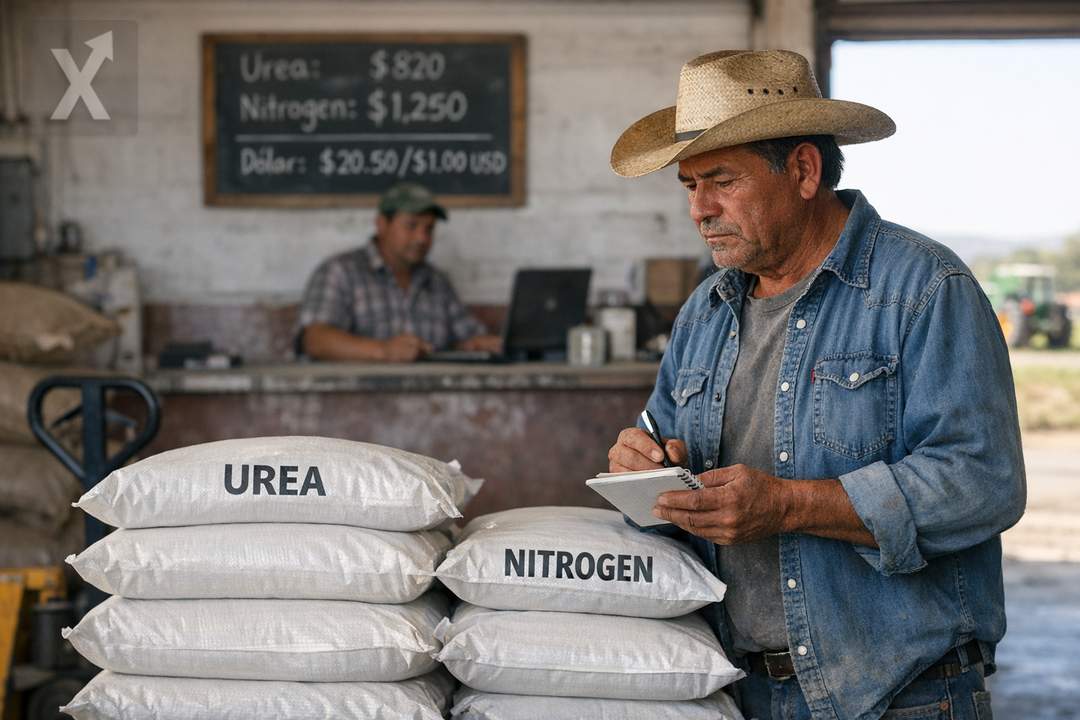

Rising military tensions in the Middle East have once again put the Strait of Hormuz at the center of global trade—and, by extension, Mexican consumers’ wallets. As marine insurance gets more expensive, routes are disrupted, and cargo availability tightens, nitrogen fertilizers—especially urea—have posted sharp gains in international markets, a shock arriving at a delicate moment for agricultural profitability in Mexico.

The problem is structural: Mexico relies heavily on foreign supply to meet its fertilizer demand, particularly nitrogen-based fertilizers used in large-scale crops such as corn and wheat. With a meaningful share of global trade in these inputs moving through Hormuz, any disruption translates into price volatility and supply risks. For Mexican producers, that means facing higher costs right at the start of key planting cycles, with margins already squeezed by weather, financing conditions, and international prices.

In agriculture, fertilizer is not a minor expense. Depending on the crop and the technology package, it can account for a sizable share of total production costs. That’s why, when the international price jumps quickly, the adjustment is often felt first in application decisions (lower doses or substitution toward less efficient alternatives), then in yields, and—with some lag—in consumer prices, especially for grains and processed foods that depend on them.

This is also unfolding in an environment where the exchange rate has shown episodes of peso strength against the USD, which in theory makes imports cheaper, but doesn’t offset the hit when the input price itself surges and added premiums appear for geopolitical risk, logistics, and insurance. For agrifood exporters, a stronger peso can also mean lower revenues in local currency, complicating their ability to absorb cost increases without raising prices or cutting investment.

At ports and across logistics chains, the effect is amplified: shipping lines and carriers typically pass higher risk and longer transit times through to freight rates. In practice, that adds another layer of pressure to imports not only of fertilizers, but also of goods tied to mass consumption, raising the total “landed cost in Mexico” even when the factory price doesn’t change.

Inflation, Banxico, and the challenge of containing the pass-through to food

The potential pass-through from fertilizers to food prices becomes especially relevant for monetary policy. Mexico’s non-core component of inflation—where agricultural and energy shocks tend to show up—is historically volatile, but when a shock drags on it can seep into core inflation through input costs, transportation, and expectations. For the Bank of Mexico (Banxico), that makes for a more complicated backdrop: even with disinflation in some categories, a sustained rebound in food prices could delay convergence to the target or keep the debate alive over the pace and size of potential rate cuts.

On the ground, the calendar works against farmers. Imported fertilizers take weeks to arrive from producing regions and strategic shipping corridors; as a result, the effects of logistics interruptions tend to be felt with a lag—right when producers need to secure supply for peak-demand stages. If high prices combine with limited availability, incentives grow to postpone purchases, which can in turn create additional spikes in local prices.

Mexico’s vulnerability isn’t only about geopolitics. In recent years, the farm sector has faced a mix of factors: water stress in agricultural regions, climate variability that hurts yields, higher energy and transportation costs, and market conditions where international grain prices can move against producers. If fertilizer gets more expensive while grain selling prices don’t compensate, the adjustment typically shows up as lower application rates or fewer planted acres, with consequences for domestic supply.

On the public policy side, input subsidies have sought to provide relief to certain segments, but they tend to be concentrated among smaller-scale producers and don’t always cover those who supply wholesale markets and agro-industrial chains more directly. In a prolonged shock, the discussion usually shifts toward how to strengthen productivity (efficient nutrient use, precision agriculture, better irrigation practices), diversify suppliers, and increase domestic production or blending capacity—while keeping fiscal costs and industrial feasibility in view.

Internationally, multilateral organizations have warned that a prolonged conflict could reinforce inflationary pressures via energy, transportation, and food. For Mexico—which imports a significant share of agricultural inputs and participates in regional agrifood supply chains—the message is clear: the risk isn’t just a temporary price jump, but a more persistent episode that affects planting decisions, yields, and logistics costs, with a direct impact on the consumer basket.

In perspective, this episode underscores how sensitive food security and inflation are to global bottlenecks. If disruptions in Hormuz ease, the market could gradually normalize; if they persist, the adjustment could show up as a combination of higher on-farm costs, pressure on food prices, and less room for maneuver for monetary policy. The key variables will be how long the shock lasts, how easily suppliers can be substituted, and how importers’ and producers’ logistics respond.

In short, higher fertilizer prices driven by tensions along strategic routes like the Strait of Hormuz are hitting a Mexican farm sector already under pressure and raising the risk that, with a lag, higher costs end up showing up in food prices and in the inflation challenge Banxico is watching.