Cetes Yields Pause Their Decline: Markets React to the Inflation Uptick and Banxico’s Path

The latest Cetes auction delivered mixed rates and a rebound at longer maturities, as inflation moved back above target and Banxico faces finer policy calls.

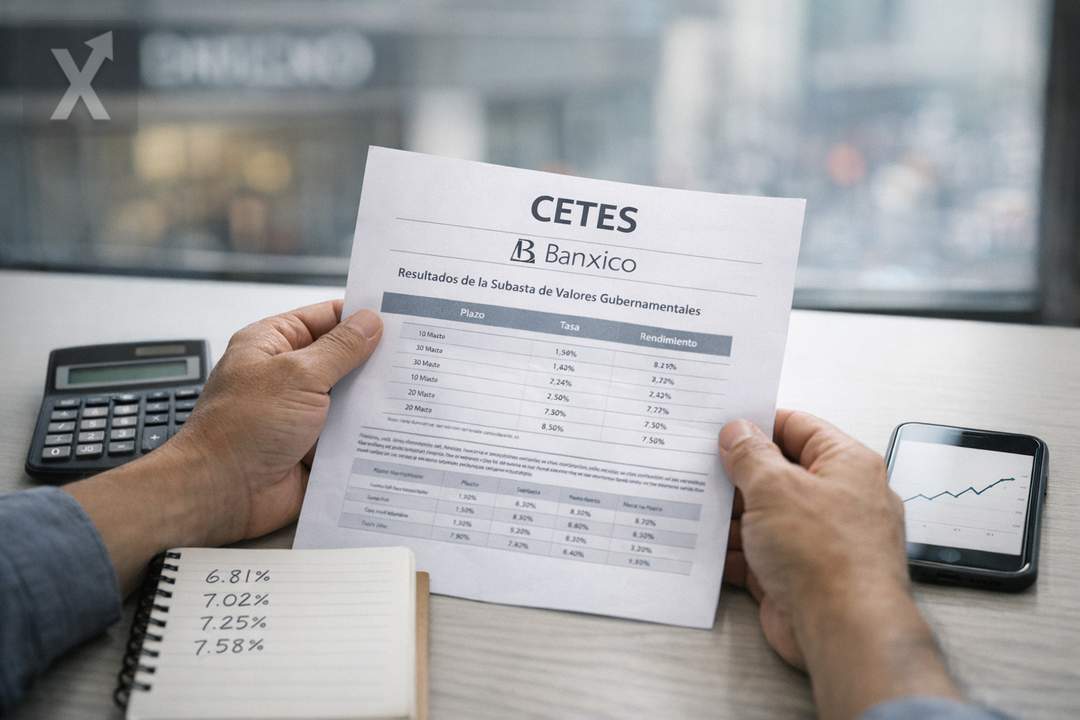

Yields on Treasury Certificates (Cetes) stopped falling across the board in the auction held in the third week of March, sending an important signal for the economic outlook: the market is still demanding an attractive premium at longer tenors after a recent pickup in inflation and amid the still-dominant expectation that the Bank of Mexico (Banxico) will continue a gradual rate-cutting cycle.

In the latest results, the 28-day Cete was essentially unchanged at 6.81%, while the 91-day instrument slipped 0.06 percentage points to 7.02%. By contrast, the 182-day and one-year tenors moved higher to 7.25% and 7.58%, rising 0.16 and 0.37 percentage points, respectively. The shift suggests that part of the market is reassessing forward-looking risks, right as headline inflation came in at 4.02% year over year in February 2026—above the 3% target +/- one percentage point.

In Mexico, Cetes have become the most accessible benchmark low-risk investment for households and businesses, thanks to their ease of purchase and because their yield is often weighed against inflation. With inflation at 4.02%, current rates still offer a positive cushion (in simple terms, an approximate “real” return), supporting demand from investors looking to preserve purchasing power without taking on high volatility.

Inflation, Expectations, and the “Price” of Time: Why Longer Tenors Are Rising

When short-term rates stabilize but longer maturities rise, it often reflects a reset in expectations: the market may be pricing in that disinflation won’t be linear, that Banxico’s cuts could be more cautious, or that the risk premium has increased given the mix of domestic and external factors. In Mexico, the inflation path depends not only on internal demand, but also on logistics, energy, and food costs, as well as the exchange rate and the monetary stance in advanced economies. That set of variables tends to matter more for 6- to 12-month yields, where investors are effectively “buying” time and demand greater compensation if they think inflation may take longer to converge to target.

For Banxico, the challenge is to calibrate the pace of monetary easing without losing anti-inflation credibility. With inflation above the target range, the central bank faces a delicate balance: on one hand, money that is too expensive cools credit and investment; on the other, faster cuts can put pressure on price expectations if core inflation—the component that is typically more persistent—doesn’t ease as quickly as expected. In that context, the Cetes yield curve works like a thermometer: if longer tenors keep rising, the implicit message is that the market sees more risks or less room to cut rates quickly.

On the fiscal front, Mexico typically retains demand for short-term government debt due to its high liquidity and perceived low credit risk; however, appetite for—and the pricing of—these instruments also responds to the global backdrop. Shifts in risk aversion, changes in international rates, and bouts of volatility can alter flows into emerging markets, moving local rates even if domestic fundamentals don’t change abruptly.

For retail investors, the practical takeaway is twofold. First, Cetes continue to offer yields above observed inflation, reinforcing their role as a defensive instrument. Second, the spread across maturities becomes more important: if liquidity is the priority, the 28-day term offers stability; if the goal is to lock in a rate for longer, the rebound in the one-year yield may look attractive—at the cost of tying up funds for more months.

Looking ahead, the key will be whether inflation confirms a downward trend in the next reports and whether Banxico maintains communication that anchors expectations. If prices remain persistent, the market may keep demanding relatively high yields at 6- to 12-month tenors; if disinflation regains traction, pressure on longer yields could ease, resuming a gradual decline in the economy’s financing costs.

In short, the March auction points to a transition phase: Cetes remain a low-risk haven with an estimated positive real yield, but the rebound at longer maturities is a reminder that the fight against inflation still shapes the direction of monetary policy and investment decisions.