Motherhood Can Also Shrink Your Pension: A Quiet Gap in Mexico’s Retirement Savings

In Mexico, maternity leave protects a worker’s income, but it can create a dip in contributions and deposits that may translate into lower pensions for women.

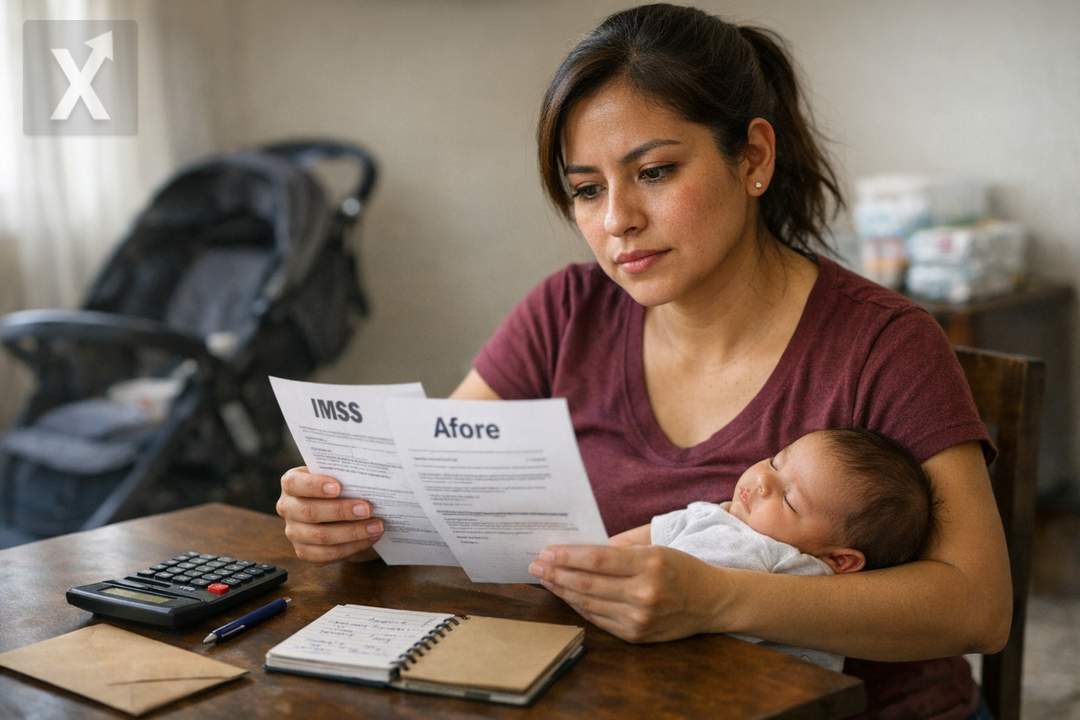

In Mexico, maternity leave in the formal sector is designed to safeguard a worker’s income: during the leave, the IMSS pays a benefit equivalent to 100% of the registered wage. However, the individual-account setup of the Retirement Savings System (SAR) leaves a blind spot: during that period, the flow of contributions to the Afore account may decrease or be interrupted, affecting the pace at which retirement savings accumulate and, in certain cases, the count of credited contribution weeks. In a system where the final pension amount increasingly depends on how much is saved and on contribution density, these pauses matter.

The problem doesn’t end with a couple of months without contributions. It combines with more intermittent work histories, a higher likelihood of informality, and lower average earnings for women compared with men. The result is a gender gap in retirement that may become more visible as more people fully retire under the defined-contribution regime (1997 Law), where you essentially “retire with what you managed to save,” and the state no longer makes up the shortfall as it did under the old defined-benefit framework (1973 Law) for those who still retain rights under it.

Different assessments of the labor market and savings point in the same direction: even among people with paid work, women show lower presence in retirement accounts and, above all, less continuity in contributions. It’s not uncommon for accounts to be opened and then go long stretches without receiving mandatory deposits due to periods of leaving formal employment, job changes, or transitions into more flexible arrangements without social security coverage.

For Mexico’s economy, the impact goes beyond the individual level. Lower retirement savings across a large segment of the population puts pressure on the debate over pension adequacy, increases the risk of future reliance on public transfers, and reduces households’ financial cushion in old age. In a country that is gradually aging and where informal employment remains high, pension adequacy has become a structural economic policy issue.

Paid leave, but with retirement-savings gaps

During maternity leave, the worker’s income comes from the IMSS benefit and not necessarily from the employer’s payroll. In practice, that can translate into incomplete or suspended contributions to certain components of retirement savings, depending on how the base contribution wage is determined and which payroll charges are actually triggered during that period. Even if the leave seems short, the effect adds up: two or three maternity events, plus any additional time off for caregiving, can reduce contribution density and the total amount accumulated—precisely in a system where every week and every peso contributed count.

In addition, some job-linked benefits—such as vouchers or other perks—often depend on each company’s policy and may not be provided during leave, reducing the household’s disposable income at a time of higher expenses. That tighter cash flow also limits the ability to make voluntary contributions, which in Mexico remain low and are concentrated among higher-income households.

Informality and caregiving: the trigger behind the gap

The main amplifier of pension inequality isn’t just the leave itself, but how the labor market responds to motherhood. Caregiving responsibilities still fall disproportionately on women, encouraging career paths that include temporary exits from formal employment or moves into informality to gain flexibility. In Mexico, informality remains a persistent feature of the labor market, and among working mothers it tends to be higher. Every month outside the social security system means fewer credited weeks, fewer mandatory contributions, and therefore a lower expected pension—especially under the individual-account regime.

This phenomenon also intersects with the wage gap, occupational segmentation, and unequal access to jobs with benefits. When income is lower or more volatile, voluntary saving becomes harder, and the individual account depends almost entirely on mandatory contributions. On top of that, women’s labor force participation in Mexico—while it has made gradual progress—remains below men’s and below what is seen in several comparable economies, limiting total lifetime contribution time.

Pension reform and the dilemma of who pays the “cost” of caregiving

The 2020 reform gradually increased the mandatory employer contribution to improve future replacement rates, on a path that continues through the current decade. On paper, this increase strengthens the savings of people who manage to maintain stable formal careers. Still, the improvement is distributed unevenly when contribution density is low: for those who alternate between formality and informality, the potential benefit shrinks.

That’s why some proposals aim to “neutralize” the impact of motherhood on retirement: recognizing those periods as credited weeks for pension purposes, or adjusting public support mechanisms (such as government contribution components) with a gender lens. The challenge is fiscal and structural: extending contributions during leave or creating explicit offsets requires defining funding sources, clear rules, and verification mechanisms—while avoiding excessive burdens on businesses or on the federal budget in a context of limited fiscal space and competing social spending priorities such as health, education, and infrastructure.

At the same time, measures outside the pension system—expanding care services, child care centers, more balanced parental leave, stronger enforcement and simplification to make formalization easier—can have deeper effects on women’s contribution density. Economically, greater continuity in formal employment not only improves expected pensions; it also strengthens the contribution base and can raise productivity by enabling more stable career paths.

In short, the current design protects income during maternity, but it doesn’t always protect retirement savings with the same consistency. The combination of contribution gaps, informality, and the caregiving burden explains why the gender pension gap persists and could widen as the individual-account system matures; closing it requires pension adjustments and, above all, labor and care policies that support continuous formal careers.