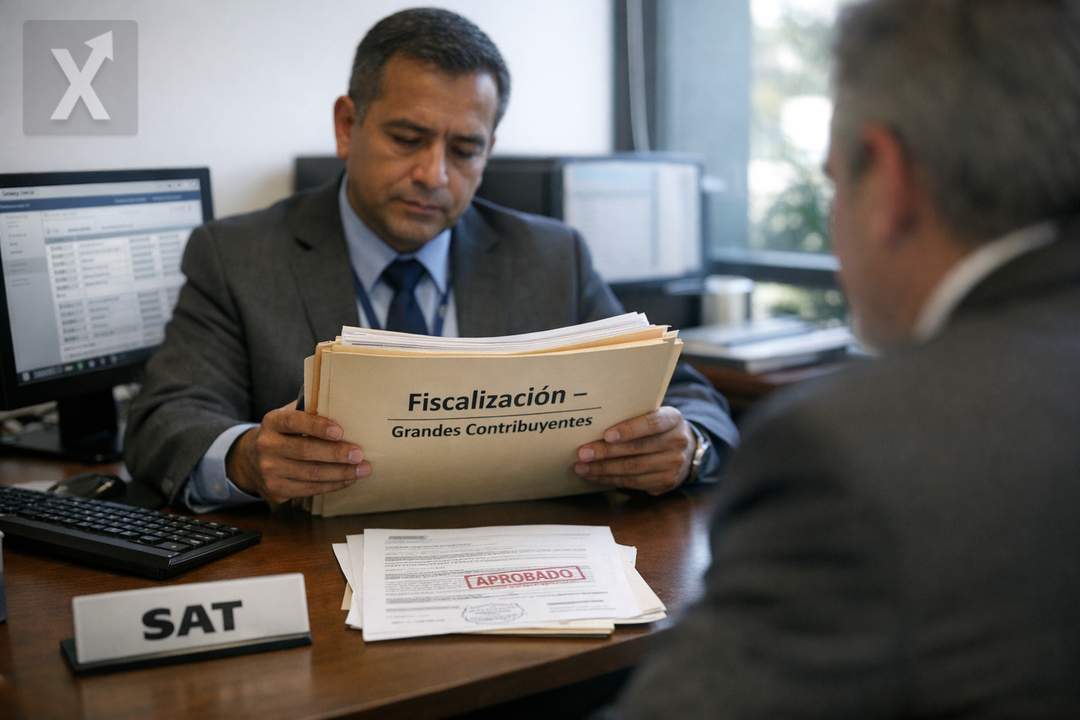

Fiscalización a grandes contribuyentes: el SAT eleva la recaudación sin subir impuestos

La recaudación por auditorías a grandes empresas se disparó desde 2020 y se volvió un pilar para sostener los ingresos tributarios sin una reforma fiscal.

La estrategia de fiscalización intensiva a grandes contribuyentes se consolidó como una de las principales palancas de ingresos del gobierno federal en México. De acuerdo con cifras de la Secretaría de Hacienda y Crédito Público (SHCP), los recursos obtenidos por actos de fiscalización a empresas con ingresos anuales superiores a 1,500 millones de pesos pasaron de 165,575 millones de pesos en 2020 a 349,970 millones en 2025, un incremento que, en términos prácticos, duplicó la aportación de este rubro a la caja pública.

El dato es relevante no solo por su magnitud, sino por lo que revela sobre el modelo recaudatorio de los últimos años: priorizar el combate a la evasión y la elusión —bajo el principio de “cero condonaciones”— en lugar de impulsar una reforma fiscal de gran calado. En un entorno donde el gasto social, las pensiones y los proyectos de infraestructura presionan el presupuesto, Hacienda ha buscado fortalecer los ingresos tributarios con mayor control, litigios y auditorías, especialmente sobre los contribuyentes con mayor capacidad administrativa y financiera.

En 2025, el monto captado mediante revisiones, auditorías, requerimientos de información, visitas domiciliarias y esquemas de “vigilancia profunda” equivalió a alrededor de 12% de todo el ISR recaudado ese año, según las mismas cifras oficiales. Esa proporción ilustra hasta qué punto la fiscalización a grandes empresas dejó de ser un componente complementario para convertirse en una fuente estructural de recursos.

La política se mantiene bajo la administración de Claudia Sheinbaum, con un énfasis adicional en analítica de datos, digitalización y uso de herramientas automatizadas para seleccionar casos, cruzar información y perfilar riesgos. El SAT ha planteado que su capacidad tecnológica permite auditorías más focalizadas, lo que reduce el margen de error y eleva la probabilidad de cobro efectivo.

Más eficiencia, pero también más controversia: el costo de litigar

Los indicadores de desempeño reportados por Hacienda sugieren una mejora en la eficacia de la fiscalización. Entre 2020 y 2025, el promedio recaudado por acto de fiscalización a grandes contribuyentes avanzó de 253 millones a 285 millones de pesos, mientras que la proporción de revisiones profundas que concluyeron con cobros superiores a 100,000 pesos subió de 69% a 75%. Sin embargo, el aumento en montos y la presión fiscal también han intensificado disputas administrativas y judiciales. Para las empresas, el entorno implica mayores costos de cumplimiento, provisiones contables y, en algunos casos, litigios prolongados; para el gobierno, el reto es lograr cobros sostenibles y defendibles sin erosionar la certidumbre regulatoria que la inversión privada suele exigir.

En la lista de grandes contribuyentes sujetos a fiscalización durante los últimos años han figurado corporativos de alto peso en la economía mexicana, incluyendo Grupo Elektra y TV Azteca, además de firmas con presencia relevante en comercio, telecomunicaciones, bebidas, banca y manufactura. El enfoque no es menor: la autoridad busca capturar brechas de recaudación donde suelen concentrarse esquemas complejos de deducciones, reestructuras, precios de transferencia o discrepancias entre ingresos declarados y flujos observables.

Para 2026, la autoridad fiscal prevé mantener el ritmo de revisiones a alrededor de 1,200 grandes contribuyentes, en línea con la lógica de que el margen de mejora en recaudación puede venir más de elevar el cumplimiento que de crear nuevos gravámenes. Esta aproximación se apoya, además, en la información creciente que generan los comprobantes fiscales digitales, las plataformas de pagos y la bancarización, que facilitan la trazabilidad de operaciones.

El telón de fondo es una economía con crecimiento moderado, alta sensibilidad al ciclo de Estados Unidos y presiones internas por el costo financiero de la deuda y las necesidades de gasto. En ese contexto, la fiscalización a grandes empresas funciona como un “amortiguador” recaudatorio: permite mejorar ingresos sin modificar tasas generales, pero también aumenta la dependencia de cobros extraordinarios y de resultados administrativos que no siempre son lineales.

Hacia adelante, el desafío para el SAT y la SHCP será equilibrar el rigor recaudatorio con reglas claras y procesos ágiles, de modo que el fortalecimiento de ingresos no se traduzca en incertidumbre para la inversión. La señal es clara: sin reforma fiscal, la estrategia seguirá descansando en eficiencia administrativa, tecnología y una política activa de auditoría sobre los contribuyentes de mayor tamaño.

En perspectiva, el repunte de la recaudación por fiscalización muestra una administración tributaria más intensiva y con mejores herramientas, pero su sostenibilidad dependerá de que los cobros sean recurrentes, transparentes y compatibles con un entorno de certidumbre para la actividad económica.