Plan México Aims to Unlock Credit for SMEs; the “First Loan” Remains the Biggest Barrier

Public guarantees and training seek to open the door to a first formal loan for thousands of businesses that still operate outside the banking system.

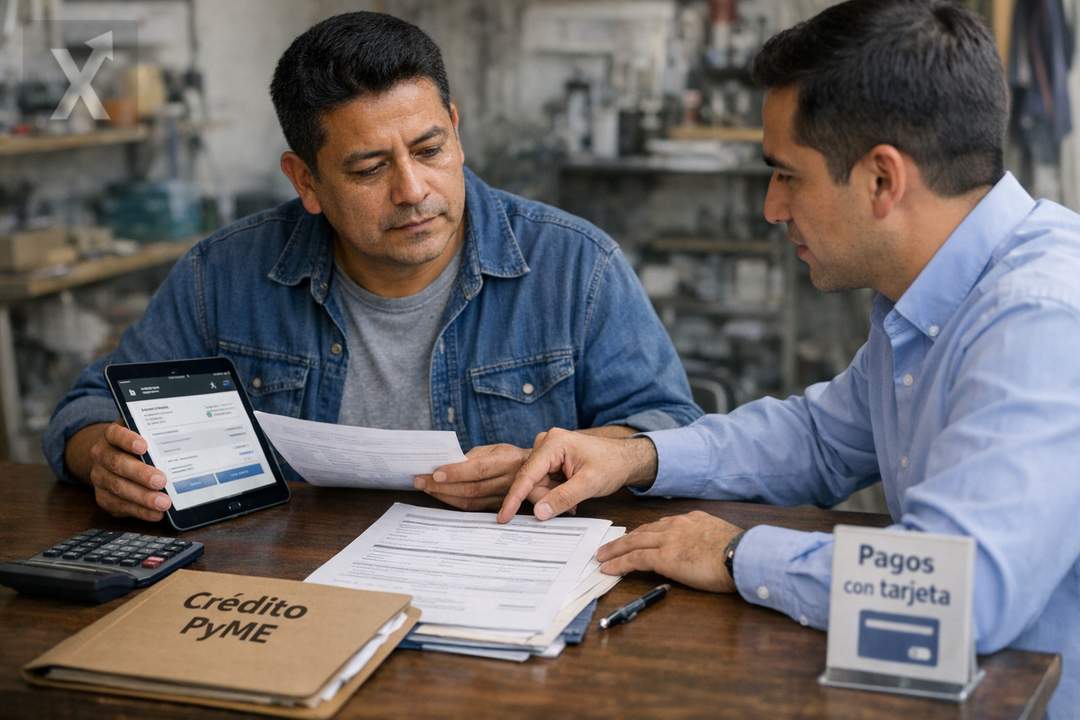

In Mexico, expanding financing for small and medium-sized enterprises (SMEs) continues to run into a structural problem: a large share of businesses has never had a bank loan and therefore lacks a credit history to prove its ability to repay to a financial institution. Against that backdrop, Plan México—an initiative designed to coordinate development banks and commercial banks to increase financial inclusion—aims to push lending to a segment that, while it is the backbone of employment, remains underserved by traditional banking.

The program’s bet is to combine public guarantees, technical support, and bank origination so more firms can make the leap from informal financing (suppliers, family, rotating savings groups, or unregulated loans) to formal credit. Among the participants, Banco Santander has set a goal of extending roughly 36 billion pesos in SME credit during 2026, which would imply about 16,000 new loans and origination growth above 20% annually, according to what bank executives have shared in meetings with the media.

The underlying challenge isn’t just “lending more,” but lending better: assessing risk with limited information, designing products that match irregular cash flows, and supporting the transition of businesses that operate with low levels of formality. For banks, the first loan is often the most complex because there are no prior references in credit bureaus, audited financial statements, or patterns of banked income; for businesses, the lack of documentation, invoicing, or business accounts limits access to competitive terms.

The effort comes in an environment where Mexico’s economy has shown resilience, but also signs of slowing in some areas, with still-high financing costs after a restrictive monetary cycle and with companies adjusting inventories, investment, and working capital. In that context, credit can serve as a cushion to sustain operations and jobs, but it can also become a risk if it is extended without training and without a realistic read of repayment capacity.

Nafin Guarantees: A Lever to Lend Where There’s No Track Record

One of Plan México’s core components is the use of guarantees from development banks—mainly Nacional Financiera (Nafin)—which in certain structures can cover around 70% of credit risk. In practice, this reduces the bank’s expected loss and makes financing viable for businesses that, due to their size or lack of history, would be excluded under traditional origination models. The goal is for public backing to function as a “bridge” to the first loan, with smaller initial amounts and clear rules so that, with strong repayment behavior, the business builds a track record and can later access loans without a guarantee or with better rates and terms.

This approach also reflects a persistent reality: productivity and formality vary widely among microbusinesses, small firms, and mid-sized companies. For many, the first formal loan doesn’t just finance inventory or equipment; it requires getting the books in order, separating personal and business finances, and starting to document sales and costs. That professionalization, while time-consuming, is often decisive for securing recurring financing and scaling up.

Training and Digitization: The Other Half of Access to Financing

Beyond the backing of guarantees, the strategy includes upfront training to increase companies’ “bankability.” In 2025, Bancomext and Nafin trained more than 81,000 MSMEs through 619 programs aimed at improving administrative management, formalization, foreign trade, and the adoption of digital tools. The logic is straightforward: a business with stronger processes, records, and practices reduces perceived risk, improves eligibility, and can negotiate better terms. Digitization—from card payments and invoicing to inventory management and reconciliation—also makes it easier for banks to evaluate cash flows using data, not just self-reported statements.

In the medium term, Plan México’s effectiveness will be measured by its ability to turn a “first loan” into a sustainable financial relationship: one where the company uses financing to increase sales or productivity rather than simply cover short-term gaps. It will also be essential to protect portfolio quality in an environment where domestic demand and private investment may be influenced by the cost of money, global uncertainty, and trends in formal employment.

For the financial system, the incentive is clear: SMEs are a large but fragmented market. Expanding the customer base with risk models supported by guarantees, training, and data can grow banking business without deteriorating portfolios. For the economy, the potential is to boost small-scale investment, strengthen value chains, and sustain employment, given that MSMEs account for most economic units and a significant share of jobs in the country.

In short, Plan México seeks to close the SME financing gap through guarantees and training, but the critical point remains turning businesses with no track record into creditworthy borrowers without compromising portfolio health. If the “first loan” becomes a doorway rather than a stumbling block, the impact could show up in greater formality, productivity, and more stable employment.