Banks and government raise the stakes on SME lending, but getting to 45% of GDP will be gradual

Bankers say the goal of expanding financing is within reach, though they warn it will depend on profitable projects, clear rules, and time to mature.

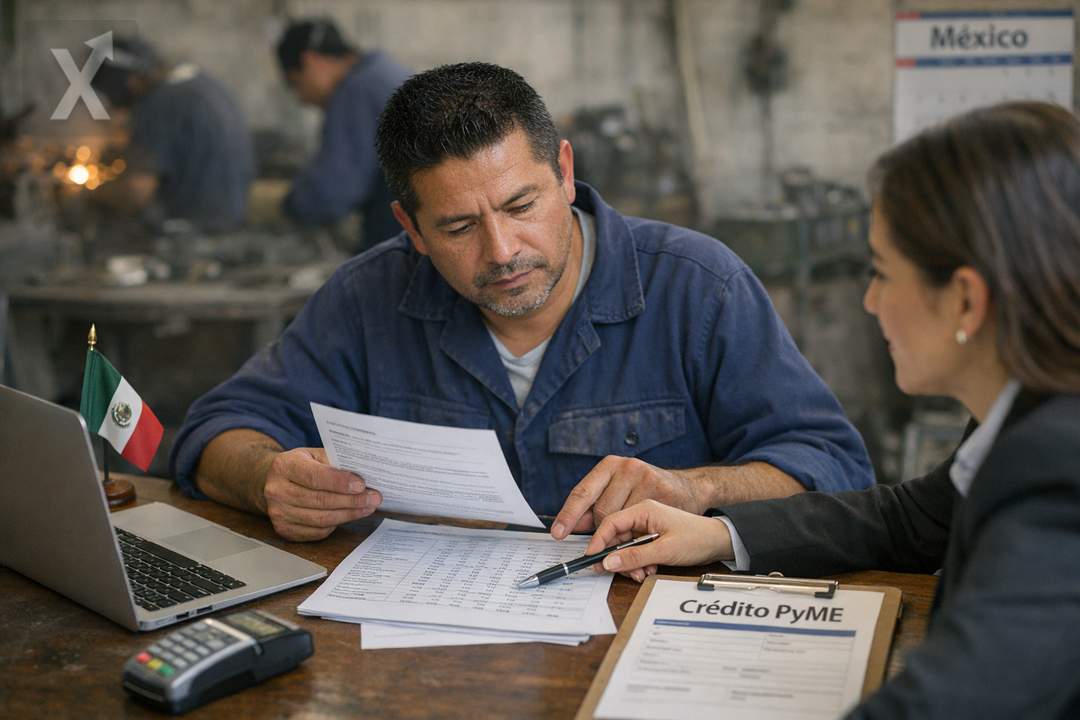

BENITO JUÁREZ, Quintana Roo.—Mexico’s banking industry agrees that the target set by President Claudia Sheinbaum—bringing financing for small and medium-sized enterprises (SMEs) to a level equivalent to 45% of GDP—is achievable, but not immediate. Industry executives say that raising credit penetration by several percentage points requires a mix of creditworthy demand, regulatory certainty, and a steady stream of productive projects, particularly those tied to infrastructure.

The proposal represents a step-change from prior commitments: the banking system had been advancing initiatives to broaden SMEs’ access to credit, and it now faces a higher bar that, in practice, calls for faster formalization, better corporate financial information, and stronger risk-mitigation frameworks. Executives interviewed on the sidelines of the Mexican Banking Convention say the goal is “challenging” because expanding credit depends not only on banks’ willingness to lend, but also on project quality and on conditions that make repayment viable.

In the background is a structural challenge: Mexico’s financial intermediation remains below that of other comparable economies, in part due to high informality, low levels of banking access in some segments, and limited income traceability for many economic units. For SMEs, financing costs also tend to include risk premiums tied to volatility, smaller scale, and dependence on consumption and investment cycles.

Bankers also underscore the role of development banks in “pushing” credit into areas where the market, on its own, moves more slowly. Guarantees, first-loss programs, and co-investment structures can reduce risk for commercial banks and lower financing costs for businesses that are currently shut out due to limited credit history or insufficient collateral. The sector’s view is that if the government provides risk-coverage tools and builds a solid project pipeline, expansion can be more orderly.

The conversation comes at a time when Mexico’s economy is sending mixed signals: on the one hand, the country retains competitive advantages from its manufacturing integration with North America and opportunities linked to supply-chain realignment; on the other, risks persist from a global slowdown, logistics costs, and domestic pressures such as insecurity along productive corridors and infrastructure gaps. In that context, SME credit becomes a key piece for sustaining investment, productivity, and formal employment.

Infrastructure and certainty: the “pipeline” that can unlock credit

One central lever for financing growth, according to the sector, is the federal government’s infrastructure agenda, which includes projects financed through public investment as well as hybrid structures with private-sector participation. For banks, infrastructure not only creates direct financing opportunities—for example, for contractors, suppliers, and regional supply chains—it also raises expected returns across multiple industries by cutting transportation costs, improving access to energy, and strengthening connectivity. However, banks caution that credit becomes activated when there is visibility: execution timelines, participation rules, payment mechanisms, and well-defined risk allocation. Without a reliable “pipeline,” financing tends to be more conservative or to concentrate on larger companies with stronger guarantees.

The goal of raising SME financing to a meaningful share of GDP also carries operational implications for the system: greater origination capacity, heavier use of analytics and alternative underwriting models (for example, transactional data), and deeper penetration of products such as factoring, revolving credit, and leasing. This is compounded by the need for financial education and advisory support for SMEs, since many require help organizing accounting, cash flow, and tax compliance—factors that often determine both access to credit and its cost.

Looking ahead, progress will depend on several fronts converging: macroeconomic stability, a predictable regulatory framework, interest rates that keep costs manageable for businesses, and public policy that encourages formalization. If these pieces align, SME credit can become a more visible engine of growth. If not, the target may be reached more slowly, with gradual gains by sector and region.

In short, banks see room to expand SME financing toward the stated goal, but they stress it won’t be a mechanical adjustment: it will require viable projects, guarantee instruments, and consistent infrastructure execution so that credit growth is sustainable and doesn’t compromise loan-book quality.