SAT Pushes Back the Electronic Value Declaration Again, Giving Importers Breathing Room Amid Customs Digitalization

The new extension to July 31 lengthens the adjustment period for importers at a time of intense logistical and regulatory pressure.

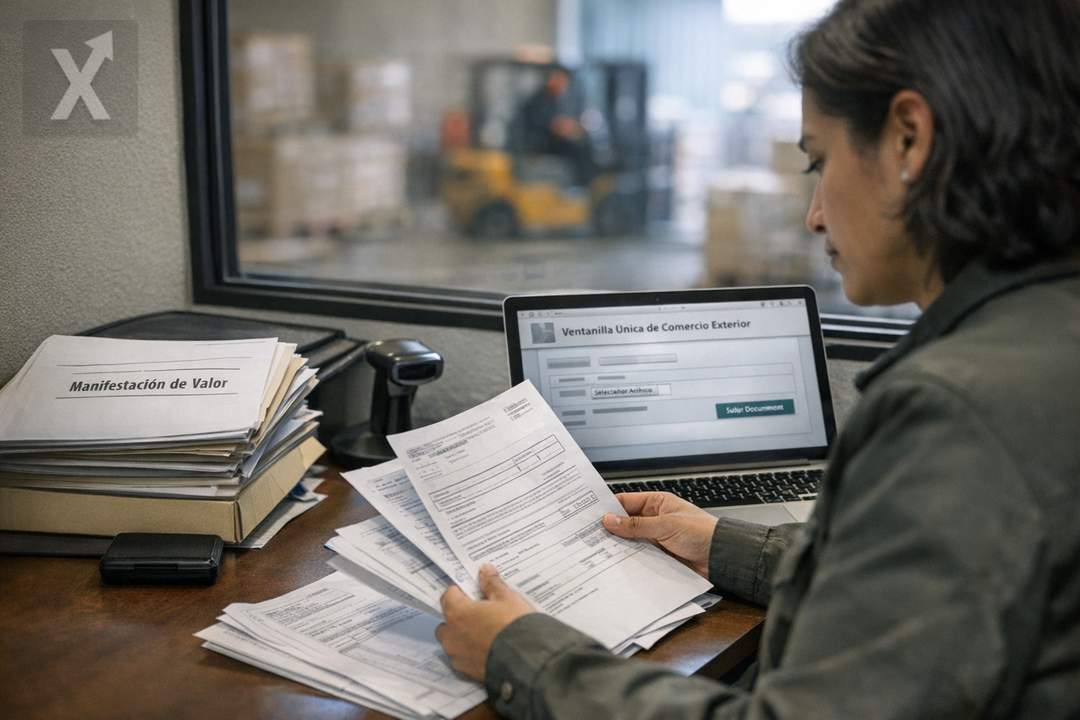

Mexico’s Tax Administration Service (SAT) has granted another extension for the mandatory entry into force of the Electronic Value Declaration (MVE), the digital file through which importers declare—under penalty of perjury—the true, complete, and traceable value of goods entering the country. According to the tax authority, mandatory compliance will be moved to July 31, after the original timeline contemplated implementation at the end of March and was later pushed back to May 31.

The adjustment underscores the operational complexity of shifting a process that has historically been handled—in practice—through customs brokers into a model where the importer more directly assumes documentary responsibility. With the regulatory change, the process is intended to become 100% digital through submission in the Single Window for Foreign Trade (VUTCE), in coordination with Mexico’s National Customs Agency (ANAM).

The MVE requires compiling and retaining digital evidence—commercial invoices, contracts, proof of payment, dutiable additions, and supporting documentation for the commercial chain, among other items—to substantiate customs value, a key input for calculating taxes, antidumping/countervailing duties, and, broadly, for supporting compliance in import operations. Authorities have said digitalization would enable faster reviews, risk mitigation, and administrative savings, though in the short term it represents adaptation costs for companies.

In an environment where Mexico maintains robust export and import activity closely tied to North America and global supply chains, the reliability of declared value becomes a critical issue: it affects tax revenue, competition among companies, and the state’s ability to detect undervaluation and avoidance practices. That is why SAT is pushing for more traceable tools and processes, while also facing the reality of uneven capabilities between large corporations and small and medium-sized businesses.

What Changes for Companies: From Paper and the Customs Broker to Importer-Controlled Documentation

The underlying shift is not just technological, but one of internal governance. With the digital MVE, importers must strengthen controls to assemble complete, consistent, and auditable files—often requiring cleanup of product catalogs, data harmonization across departments (procurement, logistics, finance, and compliance), and training for staff who feed the systems. For companies with recurring operations and multiple suppliers, the challenge grows: value traceability is not always centralized and may depend on documents issued across different jurisdictions, languages, or formats.

In that sense, the extension functions as a window to speed up digitalization efforts: scanning and archiving documents under standardized criteria, implementing approval workflows and change controls, and preparing to respond more quickly to government requests. While some companies have already adopted automation and advanced analytics to organize files and reduce errors, others still operate with scattered repositories, emails, and unstructured documents, increasing the risk of inconsistencies.

From a macroeconomic perspective, the move comes at a time when foreign trade remains a driver of growth, but also a sensitive front for tax revenue and competitiveness. Customs digitalization aligns with the global trend toward data-driven tax administration and automated cross-checks, as Mexico seeks to maintain logistical agility for “just-in-time” industries such as automotive, electronics, machinery, and intermediate goods. A rushed rollout could translate into greater operational friction; one that is too loose could dilute the control objective.

For SAT, the bet is twofold: improve information quality and strengthen risk management at customs, without slowing commercial flows. In practice, the balance will depend on platform stability, the clarity of operational criteria, and companies’ ability to meet uniform documentation standards. How coordination with ANAM evolves will also matter to avoid duplication and downtime in customs clearance.

Looking ahead, July 31 marks a checkpoint: if adoption takes hold, the country could move toward faster audits and greater certainty around declared value; if preparation or infrastructure gaps persist, compliance costs and delay risks could rise. The challenge for both authorities and the private sector will be to turn digitalization into a real efficiency gain rather than another bottleneck.

In short, SAT’s extension for the Electronic Value Declaration reflects a regulatory and technological transition aimed at greater traceability and control, but one that requires significant internal adjustments by importers to sustain the pace of foreign trade.